Q: What is GST ?

A: GST or the Goods and Services Tax is a tax on the domestic consumption of goods or services. It is tax on spending, and is not paid when money is saved and invested in a productive capacity. It is ultimately a tax on final consumption including imports, but is levied on the incremental value or value added at every stage in the production and distribution chain. It is not a tax on the seller of goods and services who simply collects GST on behalf of the Government.

Is the GST a new or additional tax imposed on taxpayers?

No. The GST is neither a new nor an additional tax. It merely replaces the Turnover Tax earlier called the Business Turnover Tax (BTT) which has been in existence in Sri Lanka since 1964.

GST and the Turnover Tax

What is the necessity for replacing the turnover tax with the GST?

Because, the turnover tax as experience has indicated, has several defects and disadvantages and the GST has relatively several ad- vantages and is superior to the turnover tax. Part of the reform of the tax system involves transforming the turnover tax to a VAT (value added tax) system.

What are the defects of the turnover tax?

The main defects of the existing turnover tax are:

i. Its ‘Cascading Nature’. Since the turnover tax is imposed on the sale price at each stage in the production and distribution chain, the price to the consumer, if it goes through a single stage, will be less than if it passes through two or more stages, as the tax paid in the proceeding stages will be added to the price in the final stage and taxed again. The price therefore depends on the number of stages.

ii. The encouragement of vertical integration of business. This simply means that in order to avoid the incidence of the tax, which is dependent on the number of steps through which a product passes from the manufacturer to the consumer, the manufacturer undertakes on his own more than one of these steps. The cascade effect therefore is either eliminated or reduced. The result is that the economies of scale and specialisation are lost.

iii. Lack of transparency. Under the turnover tax it is difficult to estimate the tax content of a price at any particular stage of production distribution Or GST Hence it is difficult to eliminate the turnover tax easily or precisely from the price, in order to provide relief to any intended sector, as for example, exports. This is because the tax is not always shown separately.

Advantages of GST

What are the advantages of the GST?

The main advantages are:

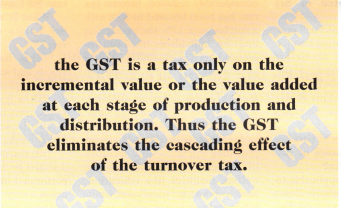

i. Unlike the turnover tax which is levied on the total turnover at every stage, the GST is a tax only on the incremental value or the value added at each stage of production and distribution. Thus the GST eliminates the cascading effect of the turnover tax.

for e.g

Input 100

Value Added 10

Output Taxable 10 (not 110)

ii. A broad-based GST does not favour any particular method of production or distribution, since at every stage what is taxed is the amount of what has been added to what has been brought in and supplied. It therefore encourages horizontal integration of businesses, with different firms specialising in different stages of production, paying tax each time one firm sold something to another.

iii. A GST properly administered with a high degree of compliance will yield the same amount of tax as now, employing fewer and lower rates.

iv. It encourages the keeping of proper records and accounts by businesses and traders. A prudent trader must always know the direction in which he is moving financially.

v. The exact amount of the tax is known at each stage, thus facilitating adjustment at any needed point.

vi. The GST has an in-built system of self-enforcement because the tax paid in respect of a transaction is deductible from the tax payable for that particular period.

This deductibility labels the supplier and provides an incentive to the recipient of the goods to declare his inputs accurately.

World-wide trend towards GST Are many countries using the GST?

GST or VAT in some form is in force in over 60 countries, 40 of which are developing countries. In Europe, it is a mandatory requirement for joining the European community. In Asia, it has spread to countries like Japan, the Philippines, Korea, Indonesia and Singapore; also to many countries in Africa and Latin America, to New GST The added Zealand And Canada amongst others. Only America and Australia, among the major countries have still to adopt it and even there it is under active consideration as a tax reform option.

GST and VAT

What is The difference between GST and VAT?

Conceptually there is no difference in principle, both being taxes on value added. In countries where it is termed the VAT there are wide ranging exemptions or zero rates to avoid regressivity and a system of multiple rates. The GST is characterized by a comprehensive base with few exemptions or zero rates and generally a single and often a lower standard rate.

Types of GST

Are there different types or models of GST?

Yes. While all are fundamentally the same in principle, in implementation there could be differences in types. For example, there are types which allow full deductions for capital goods, others which do not do so at all or allow only depreciation. In foreign trade there could be two principles – the destination principle where only imports are taxed but not exports or its opposite, the origin principle, where exports are taxed but not imports; there are also different methods of calculating the GST like the substraction method or the addition method and so on. The exact model followed depends on the conditions of each country, and the yield of tax remains the whichever method is same adopted.

What is the model or type that may be adopted in Sri Lanka?

The GST in Sri Lanka will possibly use the consumption invoice type model with full credit for capital goods and based on the destination principle where exports are zero rated. This is the model adopted by most countries implementing a GST.

Under this model will GST be applicable to all sectors of the economy in Sri Lanka?

Normally, GST is applicable to all sectors of the economy. How- ever, each country adopts a model appropriate to the conditions existing in the country at any particular time. In Sri Lanka, due to administrative reasons and the devolution of revenue authority to Provincial Councils, the GST at present is applicable only to the areas of imports, manufactures and services. The wholesale and retail trading sectors will be outside the scope of a GST and will continue to pay turnover tax to the Provincial Councils at rates fixed by them.

GST and the Population Will the GST impose burdens on the population especially the lower income group?

i. essential food, clothing and shelter being items consumed by the mass of the people are normally exempted; and

ii. a concessionary rate below the standard rate is applicable to most other goods which are semi- essential to this sector of the population.

Thus unprocessed goods and basic consumption items such as rice, bread, milk products, farm produce, drugs, housing, clothing purchased by the less affluent have little or no tax content. In contrast, the rich cannot escape from the GST unless they choose to refrain from consuming taxable goods and services.

Under the reforms made, the burden of direct taxes has been considerably reduced, income tax rate has been lowered to 35% with a surcharge of 15%, the exemption limit for individuals has been in- creased to Rs 100,000. Thus a large segment of the population either pay no direct taxes or pay taxes above a relatively high exemption limit with broad tax slabs.

The Government spends a large part of its budget annually on providing infrastructural facilities like irrigation, communications, welfare facilities like education, health, housing, vocational training and poverty alleviation schemes which benefit the less affluent sectors of the population. The effects of the GST has therefore to be viewed in this perspective.

GST and Prices

Will the GST increase prices and lead to inflation?

The GST will be designed to yield the same revenue as under the present turnover tax. It is even possible that the rates may have to be lowered below the present level so as to achieve the object of maintaining the same tax incidence. Any gaps will have to be recouped by recourse to impositions in other indirect tax areas. Impinging on the more affluent sectors of the population.

It is not taxes as such but monetary and budgetary policies that affect inflation. The experience of other countries implementing a GST indicate that the inflation rate would be lowered in the long run e.g., Indonesia, Thailand, Taiwan, Canada and New Zealand.

Scope of the GST

On what activities is the GST to be levied?

GST is chargeable,

(a) on the supply in Sri Lanka of goods and services by a registered person carrying on a taxable activity; and

(b) on the importation of goods into Sri Lanka.

What is meant by “supply in Sri Lanka of goods and services?”

This has a wide meaning. Goods and services are considered to be supplied in Sri Lanka if:

(i) the goods are in Sri Lanka at the time of supply; or

(ii) the services are performed in Sri Lanka.

(iii) the goods and services are deemed by law to be supplied or performed in Sri Lanka in special cases.

Taxable Activity

What is a “Taxable Activity”?

A “Taxable Activity’ is an activity:

(a) which is carried on continuously or regularly; and

(b) which involves supplies made to another person for the payment of money or some other consideration, not neccessarily for profit.

Taxable Activities are therefore:

(i) any trade, business, profession or vocation carried on by a person which includes a company, an unincorporated body of persons, a public or local authority including Provincial Councils, the Government of Sri Lanka, any partnership or joint venture.

(ii) Non-profit bodies associations; clubs, societies etc.

What is not a taxable activity?

A number of activities are not taxable activities. These include employment, hobbies, personal transactions, making tax exempt supplies.

Trading Sector

Are wholesale and retail traders liable to GST?

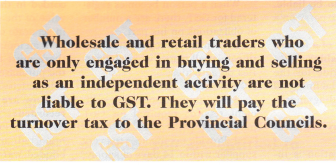

No. Wholesale and retail traders who are only engaged in buying and selling as an independent activity are not liable to GST. They will pay the turnover tax to the Provincial Councils.

Is an importer who sells wholesale and retail as an independent activity liable to GST?

No. He will include the GST paid at import in his price and reimburse himself. However, he will be entitled to issue an invoice to registered persons indicating as a separate item the amount of tax that he would have paid on that supply, so that the recipient will be enabled to claim a credit against his output tax. He may apply for voluntary registration but will have to, in addition to the GST, pay tax to the Provincial Council as a wholesaler/retailer.

If a wholesale or retail trader engages in manufacturing will he be liable to pay GST?

Yes. If in addition to wholesale or retail trade he engages in manufacturing or providing services he will be liable to GST even on the wholesale and retail sales.

Registration for GST

Who may register for GST?

Anyone who is conducting a taxable activity may register or anyone who intends to conduct such an activity. For example, if you plan to open a business you may apply for registration in advance, so that you may obtain the benefits of registration from the very beginning.

Who must register?

Everyone who:

(i) has a taxable supply in excess of a specified amount (generally much higher than the present amount) in a quarter i.e., any three months ending on the last day of the months of March, June, September, December.

(ii) has a taxable supply in excess of an amount which is not much less than that of four-quarters in respect of a period of 12 months (4 quarters).

(iii) imports goods, irrespective of the value of the import, unless the import is exempt under the Act, “Taxable Supply” means any supply of goods and services in Sri Lanka which is charged with tax pursuant to section 2 of this Act, including tax charged at the rate of zero percent pursuant to section 6 of the Act.

Exemptions

What are the supplies generally exempted from GST?

They are mainly items considered essential for mass consumption or for the benefit of the economy and normally include the following:

1. Primary agricultural produce

2. Pharmaceutical products 3. Books

4. Financial services

5. Fertilisers and animal feed 6. Passenger transport services 7. Certain educational services

8. Essential agricultural implements etc.

A detailed list will be part of the law.

Rates

What will the rates be?

The number of rates will not exceed three:

(i) a standard rate

(ii) a concessionary rate

(iii) a zero rate for exports only

Zero Rates

What is the Difference between exemptions and zero-rates?

Exemptions do who selling not the not fall within the scope of the GST and hence are not taxable. Zero rated items are in principle taxable items but the rate of tax is zero, Suppliers of exempted goods and services are therefore not eligible for refunds of GST paid on inputs, but zero rated suppliers are eligible for refunds of all input taxes paid. A final recipient of a zero rated supply therefore receives the supply entirely free from GST.

What supplies are zero rated?

Only goods that are exported or supplied in Sri Lanka to be used or consumed outside Sri Lanka. What services are zero rated? All services that are not performed in Sri Lanka.

Registration and its Advantages

How does a person register for GST?

He has to apply to the Inland Revenue Department in a pre- scribed form not later than 14 days after becoming liable to register.

Do persons already registered for turnover tax have to register again?

Yes. It is proposed to issue application forms to all those liable to be registered in advance so that they may reap the benefits of registration from the first day itself.

Can a taxpayer cancel his registration?

Yes, he can. A registration can be cancelled if he applies in writing and satisfies the Revenue that he will not continue to be liable after 12 months from the quarter in which he ceased to be liable, unless he has ceased to carry on a taxable activity.

What is the effect of a failure to register though liable?

The Act will provide for the imposition of substantial fines and prosecution not excluding imprisonment.

What is voluntary registration purposes?

Voluntary registration is intended to enable persons having a taxable supply less than the limit set for compulsory registration, to register so as to enable them to issue tax invoices and be competitive. They however, will be liable to pay GST even though the value of their supplies is less than the threshold (the amount specified per quarter for those who are liable). However they may de-register after the prescribed period of 12 months.

The desirability of opting for GST depends on each individual person’s circumstances. A person might prefer not to register if he supplies mostly to unregistered persons, if most of his customers are registered persons able to claim back any GST element in the supply price, then it will be advantageous for him to register. Other factors which may influence his decision would be:

i) the cost of complying with the legal requirements.

ii) proportion of his sales to exempt organisation.

iii) the proportion of zero-rated supplies.

iv) the profitability of the taxable activity.

v) the availabilty of a large input credit resulting from the introduction of capital assets which could result in a refund.

Obligations of Registered Taxpayers

What are the obligations when a person becomes registered?

When a person becomes registered for GST, there are a number of obligations on his part.

1. Display the registration certificate at all places where he caries on activities;

2. Notify any change of status;

3. Maintain proper and sufficient records required for GST

4. Provide tax invoices to every supplier within 14 days of supply;

5. Provide debit and credit notes when required;

6. Furnish a return within the prescribed period

7. Calculate an amount for out- put tax payable by the due date;

8. Claim credit for input tax and other deductions allowable and claim for refunds where necessary.

Records

What are the records that have to be maintained?

For GST purposes the records may include:

Books of account (on paper or in computer) , vouchers , bank, statements, invoices, tax invoices, credit and debit notes, receipts, stock records and any other documents that verify transactions or book entries.These records may have to be shown or given to Inland Revenue Officers if so required. These records have to be retained for 5- 6 years.

How should sales be recorded?

Since he is required to show the GST on a tax invoice, a convenient approach would be to record the price and tax in two separate columns.

How should purchases be recorded?

The invoices should be filed and serially numbered and recorded in the books showing the value of the purchase and the tax in separate columns.

If an input tax credit is claimed there must be a tax invoice and the purchase must be for the taxable activity.

How are imports or exports recorded?

GST is due on goods which are imported and removed from a bonded warehouse. An importer can credit GST on imports the same way as GST on his other business purchases. He should therefore keep a record of imports with a separate column for the GST. This is normally shown on the Customs documents. It is possible that the collection of GST at the import point in respect of goods to be exported will be suspended for a limited period pending proof of export. e.g., Certificates of shipment, bills of exchange, bills of leading etc. On expiry of the period of suspension, if the items are not exported the tax will be collectible and in future concessions will not be granted.

Tax Invoice

What is a tax invoice?

A tax invoice is a notice of the obligation to make payment showing certain information and includes the original customs entry form. A tax invoice verifies a registered person’s claim for the GST incurred on taxable supplies pur- chased. The tax invoice should indicate the following:

1. the words “Tax Invoice” in a prominent place

2. the supplier’s name, address and registration number

3. the recipient’s name and ad- dress and registration number

4. the date it was issued

5. the date of supply and description of goods and services supplied

6. the amount excluding GST charged for the supply, the GST charged, the total amount payable.

Returns and Taxable Periods

How must the return be furnished?

A return must be furnished not later than 15 days in the month following the last date of the taxable period.

What is a taxable period?

A period is a quarter ending on the last day of each of the months of March, June, September, December. In specific cases payment may however be made on a monthly basis, this does not alter the taxable period.

Calculation of GST

How does one calculate the tax payable?

You first calculate the output tax payable on the supply, applying the appropriate rates. Deduct the total input taxes paid and/or tax paid at point of import. The balance is the GST payable.

What is output tax?

It is the tax charged on the value of the supplies made by you at the relevant rates.

What is “Input Tax” that is deducted?

It is the tax paid by you to your suppliers on the supplies received by you and the tax levied on imports at Customs point.

Adjustments

Are there any other adjustments in calculating the GST?

Yes. There are certain adjustments that may arise in certain situations when calculating GST. They are:

Adjustments to Output Tax partial private use of goods and services

⚫partial exempt use of goods and services

⚫barter transactions (where payment is not in money)

⚫fringe benefits provided to employees

⚫bad debts recovered

⚫exported second hand goods

⚫insurance receipts assets kept after ceasing to be registered

⚫on a change of accounting basis

⚫ Partial use of private or exempt goods and services

⚫GST paid to or invoiced by Customs

Adjustments to Input Tax

⚫partial use of private or exempt goods and services

⚫GST paid to or invoiced by Customs

⚫bad debts written off

⚫a change of accounting basis

Can I claim credit for purchases of machinery or any capital items?

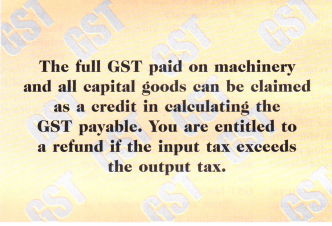

Yes. The full GST paid on machinery and all capital goods can be claimed as a credit in calculating the GST payable. You are entitled to a refund if the input tax exceeds the output tax.

Refunds

When is GST refunded?

Inland Revenue will refund. GST when:

1. the GST you have paid is greater than the GST collectible.

2. you have ceased to be liable.

In the case of 1 the claim must be made within three years of the end of the taxable period in which the refund arises. In the case of 2 a lapse of one year is necessary from the end of the taxable period in which you ceased to be liable. In the interim you will be entitled to a set-off against the liability of each succeeding quarter. At the end of the fourth quarter any excess will be refunded.

When are refunds not paid?

When:

a) a refund or part of a refund is used to set off any other taxes due and unpaid.

b) a return has not been filed, the refund may be withheld till the return is submitted.

e) the Inland Revenue is not satisfied with the return.

Imports

How is GST claimed on imports?

GST on imports is levied and collected by the Director General of Customs on the c.i.f. value the Customs Duty. The amount so paid is treated as an input tax and fully deductible in the quarter in which it was paid provided the import was in respect of a taxable activity.

By what date is the GST payable?

GST is payable not later than 15 days after the end of a taxable period which is a quarter, unless the value of supplies in the preceeding quarter exceeds five. million rupees when payment will be made monthly on the 15th of each succeeding month on the value of supplies less inputs in that month.

What happens if a return and/ or payment is not made or made later than the due date?

Under the Act, delayed payments will be subject to a 10% penalty arising on the payable date and 2% for each succeeding month or part thereof subject to certain limitations.

Failure to file a return can result in the imposition of a penalty or prosecution in the Courts. The penalties including imprisonment can be severe.

Assessments

Under what circumstances could Inland Revenue issue a notice of assessment?

1. when you or the Inland Revenue are not satisfied with the return filed. For example, if you find that your returns are wrong, you can write and ask the Inland Revenue to amend it; or

2. you fail to file a completed return; or

3. a non-registered person charges GST on supplies.

Is there a time limit for assessments to be made?

Yes. Within three years of the end of a taxable period e.g. taxable period ending September 30, 1995, statutory limitations commences October 01,1998. In the event of fraud etc., no statutory limitation applies.

Does the GST law provide for self assessment?

Yes, as for the Turnover Tax.

Appeals

Could a taxpayer appeal against an assessment?

Yes. Within 30 days, the appeal must be accompanied by a return.

Offences and Penalties

What are the other offences and penalties which a taxpayer may become liable under the GST law?

There are a wide range of offences which are provided in the GST Act. They include: failing to apply for registration as required

⚫failing to furnish returns or required information furnishing false and incorrect returns or information

⚫failing to maintain or falsifying records required to be kept for GST purposes.

⚫knowingly issuing a false tax invoice on a supply

⚫failing to pay within the prescribed period

⚫fraudulently obtaining refund

⚫Penalties vary for different offences. These include fines ranging from Rs 25,000 to Rs 50,000 or imprisonment (or both) or the charging of penalties in cases of evasion or fraud up to three times the amount of the GST involved.

Tax withholding Can tax be with held when payments are made under a contract?

The provisions as they now apply in the case of turnover tax are incorporated in the GST law.

Powers of Search etc.

Does the GST Act provide for powers to search buildings and places?

Yes.

Are there any changes to the Turnover Tax law relating to administrative and enforcement aspects?

No. The GST law is only an extension of the provisions relating” to the imposition of the tax. (courtesy: GST Development Unit)