A dramatic period of surging inflation led to the sharpest tightening of monetary policy in decades. Is a radical rethink by central banks required, or do current targets and toolkits suffice?

A dramatic period of surging inflation has led to the sharpest tightening of monetary policy in decades. Is a radical rethink by central banks required, or do current targets and toolkits suffice? Inflation is on the high side globally, sometimes more than expected. Central banks are tightening interest rates intending to curb inflation and drive it to a target of two percent. The challenge before the central banks’ task of reducing inflation is enormous, given that the events will not induce a further economic downturn and financial instability. For governments around the world, inflation has been a complex message to deliver to their people who are likely to lose confidence under the burden of rising prices. The various scenarios that global economies endured and their decisions and future strategies were the focus of scholars, central bankers, and bankers at a forum on the future of monetary policy. Hosted by CNBC and Anchor Joumanna Bercetche, the panelists were Thomas J. Jordan, Chairman of the Governing Board, Swiss National Bank, Lawrence H. Summers, Charles W. Eliot University Professor, Harvard Kennedy School of Government, Kjerstin Braathen, Chief Executive Officer, DNB ASA, and Julio Velarde, Governor, Central Bank of Peru.

January 20, 2023. Jennifer Paldano Goonewardane.

Expansionist Monetary Policy

The experts have spoken. Inflation, the buzzword sending shockwaves across economies, among policymakers and central bankers, has underestimated its pressure in 2021 amid the raging COVID-19 pandemic and its fallout. Many are quick to point to the war in Ukraine as pushing the global economy pell-mell. While no one disregards the impact of the war as the big economies try to negotiate its intricacies to minimize its effect through tightrope-walking consultations with warring parties, Jordan pins down the chaos to an over-expansionist monetary policy that drove inflation higher. Jordan points to a triad of over-expansionist monetary policy combined with fiscal policy and negative output that drove inflation upwards, demonstrating its negative impact on economies, especially its adverse impact on lower-income groups. With much insight into the situation today, the monetary policy directions in response to the crisis said Governor Jordan seems to have been “all over” in addition to being over-expansionist. Therefore, central banks must focus on reining in prices to maintain the purchasing power of their currencies, so that economies can be back on the road to stable growth.

Longer-term spending in the economy is seeing a drop, with people spending more on short-term durable goods than on long-term investment, making spending less sensitive to interest rates while increasing the possibility of volatility in actual interest rates.

A New Inflationary Paradigm in the Case of the USA?

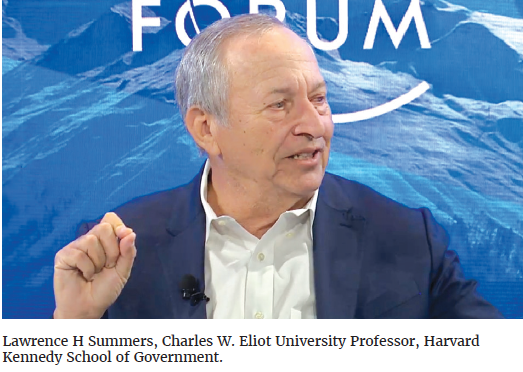

In 2013 Lawrence H. Summers, serving today as Charles W. Eliot University Professor at Harvard Kennedy School of Government, stimulated extensive interest by stating that the advanced economies were in a new era of secular stagnation. His theory propounds that more saving over investing affects demand, reduces growth, and increases inflation. The imbalance between savings and investment brings down interest rates coupled with the lack of an aggressive government fiscal policy, as the primary causes of a state of economic stagnation, where there is little noticeable economic growth. Following Summers’ description of the secular stagnation era, many analysts wondered whether a new era was unfolding with the pandemic as the US government introduced new fiscal stimulus to overcome the economic slowdown caused by the pandemic. Summers in 2021 warned of the inflation risk of an expansionary fiscal policy sans restraint, with the injection of money into the economy driving demand upwards and thereby generating high inflation.

Summers gave his verdict – it is unlikely that the US economy will return to a low-interest rate era characterizing secular stagnation. Summers was confident when he declared that the US was in secular stagnation in 2013. And in 2021 went on to warn about rising inflation with pandemic-driven government fiscal stimulus but does not see a basis for the nature of the next era revealing itself yet. Hence he warned central banks from resorting to excessive forecasting of future behavior lest it dents their credibility, instead calling them to focus on gauging the moment and resorting to doing the right thing as circumstances would deem at a given moment in time. Somewhat noncommittal about the Fed’s interest rate hikes, Summers argued that the many scenarios point to interest rates ending up higher, as historically, the path to meaningful inflation management has come from raising interest rates. He predicted less sensitivity of economic activity to interest rates, however. Longer-term spending in the economy is seeing a drop, with people spending more on short-term durable goods than on long-term investment, making spending less sensitive to interest rates while increasing the possibility of volatility in actual interest rates. That, he said, brings to the fore the argument of whether governments should drive fiscal policy more actively in their stabilization policy.

The Case of Norway

To say that tightening monetary policy and increasing interest rates did not surprise the Norwegian banking sector would be an understatement, according to Kjerstin Braathen, Chief Executive Officer of DNB ASA. In the face of rising inflation, the Norwegian Central Bank began hiking interest rates in September 2021, accelerating it in the autumn of 2022 to 2.5 percent, an increase of 0.25 percent, as inflation was edging higher than expected. The central bank had deemed it necessary to tighten monetary policy on time to curb the effects of inflation on households and businesses that were increasingly hampered in decision-making by rising costs. On its part, the central bank could justify its move, lest inadequate tightening lead to further inflation that would demand further rate increases. For banks such as DNB ASA, the tightening and increases came as a surprise, initially doubled down by their inability to predict the outcome. However, she said that today, it was easier to justify the central bank’s move to increase interest rates as inflation began escaping beyond the two percent target.

Amid interest rate increases, Norway’s floating rates on borrowings get naturally integrated into the credit market, meaning transmitted to borrowers. Bankers like Kjerstin consider floating interest rate structures contributing to monetary policy efficiency. However, its vulnerabilities could lead to undesired outcomes, especially for consumers facing budgeting constraints amid unpredictability. For corporates, the fear is its impact on liquidity position and stock prices.

Kjerstien pointed out that the Norwegian Central Bank has not wanted to move into a negative interest rate. Henceforth, it directs efforts to keep inflation low and stable and, over time, targets to reach an inflation rate of close to two percent. In a reality where banks coexist with the economic environment, increasing interest rates will demonstrate its intended outcome only if it does not kill growth in the long-term. In the short-term increased interest rates are acceptable if it does not compound issues by giving way to instability and losses of a magnitude that surpasses the increase in interest rates. She projected that Norway and Europe would continue the tightened monetary policy stance until they could tame inflation to their targeted rates.

Peru’s Monetary Policy Rollout amid Political Unrest

Many analysts saw Peru’s political unrest as dangerous to the country’s financial sector and economic growth. However, the Governor of the Central Bank of Peru, Julio Velarde, sees the political unrest as just one factor that may somewhat impact the economy and cause economic pressures while acknowledging that Peru is a country used to political instability regularly while managing to keep inflation at a low point in the interim. He reiterated that political unrest was not the main factor driving inflation. However, the central bank took a step back from tightening interest rates further but not reducing either in the face of heightened political unrest. He pointed out that while many economies wait and watch the Fed’s reaction to a phenomenon, that was not true of Latin America and Europe during the pandemic-driven economic fallout when they were the first regions in the world to increase interest rates. He said that it was an accepted practice for many economies, especially the emerging ones, to wait for the Fed’s response to a common scenario. For instance, he said that in the aftermath of the pandemic, when the Fed’s monetary policy focused on curbing inflation, which the rest of the world was battling, it was not unusual for other countries to react accordingly and hike interest rates. Global central banks coordinate when their respective economies face similar circumstances because decision-making by the Fed and other central banks can especially bear upon emerging economies.

Intervention is paramount as countries navigate a volatile future, with comprehensive approaches to support debt-ridden countries, credibly including debt and maneuvering around it is the most critical debt-related challenge.

On future monetary policy direction projection, Governor Velarde said that in Peru and Latin America generally, monetary policy will unlikely be easing, with high-interest rates remaining unchanged to tame inflation.

Future scenario for Switzerland

Describing the fight against inflation as a formidable role of defending the credibility of central banks, the challenge of bringing down inflation to a mandated two percent of price stability while not sending the economy into recession and further downturn, Governor Jordon contended that there would be a swift decline in headline inflation as energy prices reduce. In contrast, core inflation will continue slowly. Hitherto interest rates in Switzerland had been in the negative territory until 2022 when the SNB increased interest rates first time since 2007 and twice more in 2022. As inflation remains elevated in Switzerland, above the level of price stability, bringing it back to a targeted two percent could be challenging, with Governor Jordon indicating that the SNB will resort to future rate hikes to ensure price stability that he considers is the absolute priority of all central banks right now. Governor Jordan defended SNB’s negative interest regime that prevailed since 2015 amid global upheavals, claiming that returning to it is always an option when the country achieves negative inflation.

Governor Jordon pointed out that inflation-driven price increases were already underway in Switzerland, with firms responding to price increases in raw materials and energy by correspondingly increasing the prices of their goods. At the same time, wages have not seen an upward trend in tandem with the realities of the increased cost of living. There is pressure in Switzerland to adjust salaries to suit the current circumstances, especially from trade unions, as the SNB determines wages on the preceding year’s inflation rate, which employers are most likely to resist citing the uncertainty surrounding them, a sign of the challenges that it will face in bringing down inflation to a goal of two percent. The SNB intends to continue focussing on curbing the transmission of inflationary pressure on goods and services while keeping the Swiss franc strong.

Is it time to reconsider Central Bank mandated two percent target?

As many voices question the reality of a two percent inflation target for economies, and with suggestions of revising that, Lawrence Summers had a warning. He said it would be a grave error for central banks to adjust their two percent inflation targets upwards at this point and was opposed to the idea of setting a specific numerical inflation target by the United States. The Fed has repeatedly re-emphasized its commitment to the two percent inflation target. However, it still needs to attain that goal, and announcing that it would abandon that target would make a severe dent in its credibility, said Summers. He argued that resorting to an adjustment once would not be the end, the Feds could repeat that practice in the future too.

He argued that the often-heard rhetoric surrounding inflation reduction, that it’s not worth having a recession to reduce inflation misunderstands the counterfactual. The counterfactual argued Summers is not “can we have more inflation and not have a recession.” The counterfactual is that failing to deal with inflation will likely give way to a more significant and more severe recession at some subsequent point. Even if the only dominant priority was maximizing the average employment level over the next decade over the inflation rate, he argued that maintaining a commitment to price stability would be appropriate. Over time, the two percent inflation goal has come to represent the average inflation for the country. Today, with nearly seven percent inflation, no calls suggest going below two percent to achieve an average. In fact, Summers said that the Fed has been adjusting the target to the high side, indicating a degree of flexibility towards veering from the goal, which he deemed as the appropriate measure taken by the central bank.

But he asserted that what happens in the real economy is beyond the macroeconomics classroom lessons and that monetary policy alone does not determine the outcome in the real economy. Summers warned that to suppose that a degree of relenting on an inflation target will be salvation would be a costly error that will ultimately have adverse effects as it did during the 1970s for real economies and working people everywhere. Summers predicted that the Fed would likely tighten rates in the future, which he said would be for the economy’s good, as the Fed had been resisting the move for far too long.

Clash between Monetary and Fiscal Policy

Britain became the poster child of how fiscal policy got in the way of monetary policy, unfunded tax cuts as a fiscal stimulus by the government versus tightening rates by the central bank, blurring the strong complementarities between the two, rather than interact, pursuing opposing purposes rather than coordinating. In Britain, the intended fiscal policy stimulus to support vulnerable groups in society was counter tandem with the central bank’s monetary policy on a rate tightening spree. The danger pointed out by Kjerstien is that politicians in government, as elected representatives of the people, make decisions to buttress the population and maintain trust levels at a high point and need to reconcile their stimulus measures with the economic realities that central banks grapple with. Such fiscal stimulus only leads to higher market volatility and inflation demands, further tightening monetary policy to achieve the required inflation targets.

Rethinking Investment by SNB?

The forum’s moderator questioned SNB’s wisdom in investing in stocks that did not bring the desired yield but drove losses upwards. In 2022, the SNB posted a loss of $143 billion, the biggest in its 115-year history, as falling stock and fixed-income markets hit the value of its share and bond portfolio. Governor Jordon defended SNB’s investment strategy as a bid to expand its balance sheet amid a strong Swiss franc. He said that the setback overlooked the gains of previous years, the most recent being in 2021, when it made a profit of 26 billion francs. He contended that the loss-making scenario was a knockout effect of hiked interest rates leading to a weakening of global stock markets, falling bond prices, and a strong Swiss franc leading to exchange rate-related losses. Governor Jordon defended the composition of SNB’s balance sheet, asserting that there was no proof of it being irrational and predicting a more significant loss had the central bank not invested in stocks. The SNB, he said, will continue this strategy in the future.

What more Looms in the Background?

On the problem of debt compounding the situation for developing countries on top of inflation and higher interest rates, Governor Jordon said high debt diminishes the resilience of economies, households, and more, contending that economies should push for reasonable levels of public and household debt. The reality is that a government not saddled by heavy debt places itself in a stronger position to react to shocks that stir the economic status quo. A weak fiscal situation and high debt give a country limited space to maneuver, amplifying its vulnerability to increasing interest rates. He suggested that the Swiss mechanism of a Debt Brake to manage government spending to prevent deficits and thereby prevent an increase in debt is a sound system for other economies to explore and practice intermittently.

Summers warned that a combination of an increase in interest rates, a stronger dollar, oil prices, possible global recession, the continuing burdens of the pandemic, and climate change have created a near-perfect storm for many of the poorest countries in the world. Intervention is paramount as countries navigate a volatile future, with comprehensive approaches to support debt-ridden countries, credibly including debt and maneuvering around it is the most critical debt-related challenge he sees looming ahead.